The signal that matters more than your win rate

Dana White once said something that stuck with me. Talking about why UFC ratings exploded during the pandemic, he pointed out that bettors gravitated to the sport because there was nothing else to gamble on, and once they started watching they fell in love with the product. The throwaway business observation contained a betting truth I think about often: punters who stick with UFC long-term tend to develop a specific skill that separates them from casuals. It’s not picking winners – it’s picking sides before the market figures out the same thing.

That skill is what closing line value measures. CLV, as it’s known, compares the price you took on a bet to the price the same bet closed at when the market ended (i.e., when the fight started). If you backed Fighter A at 6/4 and the closing price was 5/4, you got CLV – the market moved toward your side. If you backed Fighter A at 6/4 and the closing price was 7/4, you got negative CLV – the market moved against you. CLV is the difference, and over time it’s a better predictor of long-run profitability than win rate.

That last claim deserves explaining because it sounds counterintuitive. Surely winning is what matters? In the long run, yes – but win rate has too much variance over short samples to be a reliable signal of skill. CLV reflects whether your decisions were better than the market consensus at the moment you made them, regardless of how the specific fight played out. The biggest underdog winner in UFC history closed at +950 American (9.5% implied probability) and won. Anyone who backed her at +800 in the morning had negative CLV against the closing line – they got worse value than the close – even though they won the bet. CLV and win-or-lose are independent dimensions.

What CLV actually measures and how to calculate it

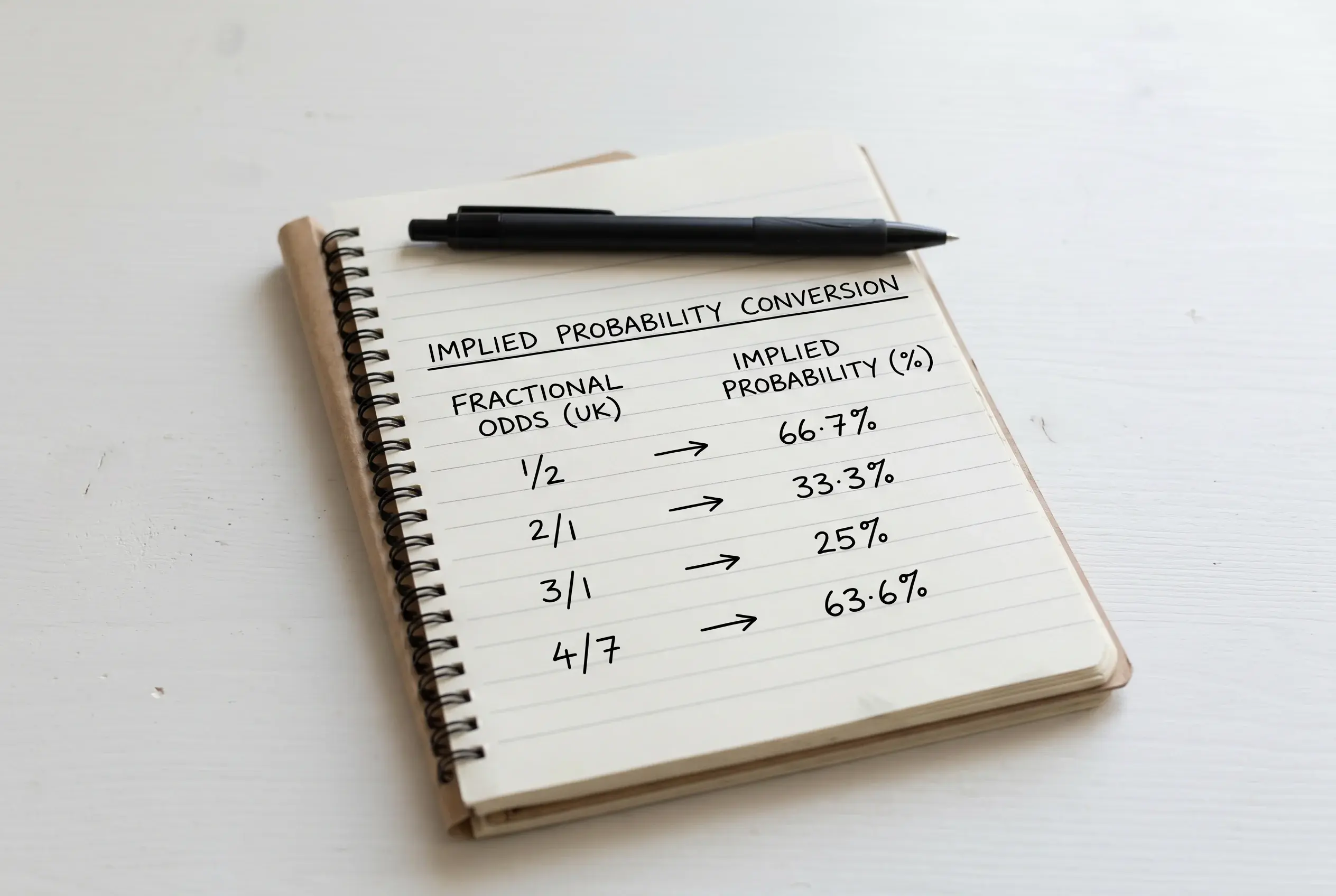

The mechanics are simple. You record the decimal odds you took on a bet when you placed it. You record the decimal odds the same selection had at the moment betting closed on that market (or as close to the start of the fight as possible). CLV is the percentage difference between the two prices, expressed as a positive or negative number.

If you backed Fighter A at decimal 2.50 and the closing price was 2.30, your CLV is (2.50 – 2.30) / 2.30 = 8.7% positive. You took a price 8.7% better than what the market settled at. If you backed Fighter A at decimal 2.50 and the closing price was 2.70, your CLV is (2.50 – 2.70) / 2.70 = -7.4% negative. You took a price 7.4% worse than the close.

Doing this on every bet sounds onerous but it isn’t really. A spreadsheet with three columns – selection, price taken, closing price – populates in 30 seconds per bet. Over 30-50 bets you have a meaningful sample and can calculate average CLV across all your activity. Positive average CLV over a sustained sample is the strongest evidence I know that a punter is actually making good decisions.

The reason CLV correlates with long-run profitability is straightforward. The closing line is the market’s best estimate of true probability after all available information has been priced in. Beating the closing line consistently means you’re identifying selections the market hasn’t fully priced when you take them. Over hundreds of bets, the gap between the prices you take and the prices the market eventually arrives at translates into positive expected value, even if any single fight result is random.

How UK books set opening lines and why they move

Closing line value as a concept depends on understanding how opening lines work in the first place. UK sportsbooks typically post UFC main-event opening prices 5-7 days before the fight. The opener is the trader’s best guess at fair odds, with margin added, before any betting volume has shaped the market.

The model inputs for the opener – power ratings, recent form, durability, weight class baselines – are reasonably standardised across major operators, which is why opening prices on the same fight at different books tend to cluster within a few percentage points of each other. The opener is the trader’s pre-market guess; everything that happens to the price after opening is market response.

Volume reshapes the opener. If sharp action piles into Fighter A at the opening price, the trader shortens A’s price to discourage further action and lengthens B’s price to attract balancing money. If recreational action piles into Fighter B (often the popular fighter or the one with the bigger name regardless of underlying probability), the trader resists moving the price too far because they don’t want to give the sharp side better odds against the unbalanced book.

The shadow line – the price the most respected sharp accounts are willing to bet at – is what trading desks really watch. When the shadow line and the displayed price diverge meaningfully, the displayed price will move to converge. Sometimes this happens fast (a quick three-tick adjustment within an hour); sometimes slowly (drift over 24-48 hours).

By the time the market closes – typically when the fighters walk to the cage – the price has absorbed most of the information the market has about the bout. The close represents consensus. Beating the close means you saw something the consensus eventually agreed with.

What drives line movement during fight week

The price between opening and closing moves for predictable reasons. Knowing them lets you spot opportunities to take prices that haven’t yet fully absorbed an information event.

Sharp money. The largest and most coordinated influence on UFC prices is sharp betting accounts piling onto a specific side. These accounts get respect from traders precisely because their CLV record is strong – when they bet, the line moves. Following sharp money is hard because the accounts themselves are opaque to retail, but the price action telegraphs it. A line that lurches 15-20% in one direction in a few hours, especially mid-week when retail volume is light, is usually sharp.

Weigh-in news. The Friday-before-Saturday weigh-in is the single biggest information event of fight week. A fighter missing weight, looking drained, or unable to make the contracted limit causes immediate line movement. Sometimes the bout is converted to a catchweight, sometimes one fighter is fined or stripped of bonus eligibility, sometimes the fight is rebooked. The biggest underdog winner in UFC history, Shana Dobson, won her +950 fight in 2020 – but the weigh-in dynamic for that bout factored into the closing line, and punters who bet earlier in the week got a different price than those who waited.

The 6.7% weight cut figure UFC athletes hit in the 72 hours before weigh-in matters here too. Fighters who appear gaunt at the official weigh-in have given up the easy weight; the question for the line is whether they can rehydrate the 9.7% body mass they typically regain in the 24-36 hours after weigh-in. Visual cues from the weigh-in shift lines materially.

Public money piling in late. The 24 hours before a fight see a surge of recreational volume, mostly piling onto the favourite or the popular fighter. Traders often lengthen the underdog’s price slightly to attract balancing action and shorten the favourite’s price slightly to discourage further favourite money. Sharp punters watching this dynamic will often bet underdog at the lengthened price in the final hours, knowing the close will tighten back.

Injury or withdrawal scares. Reports of a fighter being ill, injured during fight week, or pulled by the medical commission cause sharp movement. These are usually credible but occasionally false alarms – and the lines often overshoot when the news first breaks before correcting once the news is verified or dismissed.

Measuring your own closing line value over time

The discipline of tracking CLV on your own bets is the most valuable habit any UFC bettor can build, full stop. It tells you whether you’re getting better, getting worse, or just running good or bad on results that don’t reflect underlying skill.

Practical workflow: keep a simple bet log. Date, fight, selection, decimal odds taken, decimal closing odds. Add a column for CLV percentage calculated as (taken – closing) / closing. Add a result column (W/L). At the end of every month, average your CLV across all bets. Plot it against time.

A positive average CLV over 50+ bets is genuinely good. Over 100+ bets, sustained positive CLV is rare and reliable evidence that your decision-making is better than market consensus. Even 1-2% positive CLV average is meaningful – over a year of betting, that’s a multi-percent edge against the market.

Negative average CLV is also informative. It means your sides have, on aggregate, been worse than the market’s eventual settlement. You might still win bets in the short term – variance does what variance does – but in the long run, negative CLV translates into losses. If you’re seeing it, it’s worth examining your selection process.

The trap in CLV tracking is being selective about which bets you log. Punters often remember their winners and forget their losers, or log the bets where they took an obviously good price but not the ones where they bet on tilt. The discipline only works if every bet goes in the log.

The other trap is treating CLV as the only metric. CLV measures decision quality against market consensus, but the market consensus can also be wrong – particularly on niche markets, prop bets, and prelim Moneylines. A punter who beats the close on prelim moneylines might still be losing if the closing lines themselves are wrong. CLV is the best single metric for mainstream markets.

Why recreational bettors should still care, even if differently

If you’re betting £20 a card for entertainment, CLV might feel like an over-engineered concept. There’s some truth to that – the absolute pound amounts at stake don’t justify spreadsheet maintenance for many punters. But the underlying habit of paying attention to where prices are relative to where they end up is useful even at recreational stakes.

The simplest version: notice when a price you considered earlier in the week has moved significantly by fight night. If you almost bet Fighter A at 7/4 on Wednesday and you see the close at 5/4 on Saturday, the market agreed with your read. Not betting cost you value. Worth knowing for your own learning, even if you didn’t profit. Conversely, if you backed Fighter A at 7/4 on Wednesday and the close drifted to 2/1, the market saw the bet less favourably than you did. That’s not necessarily wrong – the market is wrong sometimes – but it’s information.

For UK sportsbooks specifically, recreational accounts that consistently beat the closing line by significant margins sometimes get treated commercially differently – stake limits applied, certain bonus offers restricted. This is operator policy, not a regulatory matter, but it’s worth knowing. Punters with sustained positive CLV at the highest levels eventually feel the squeeze. Most recreational accounts never get close to that threshold and have no reason to worry about it. One adjacent question worth understanding: UFC price boosts and enhanced odds are marketing tools UK operators use to attract action, and reading whether a boost is genuine value or repackaged margin is part of the same CLV-aware discipline.